Asset Management Information System

Asset Management Information System is defined as the use of information and communication technology, which include data acquisition and processing, software, and hardware that are necessary to provide an essential support system for an effective asset management in an organization.

The use of electronic based system has become more apparent in a big and widespread organization, which need real-time, online and future information for optimized decision-making. The need to have an electronic based information system will depend on the following factors:

- The cost of development

- The cost of acquisition and maintenance

- The expertise needed

- The benefits that will be derived from the information system

The information system will be a non-physical asset except for the hardware and have to be managed in line with asset management principles. However, in the United Kingdom’s asset management requirements as in PAS 55-1, the information system is a pre-requisite to an effective asset management as defined below:

4.3.1 Asset Management Information System

The organization shall establish and maintain (an) asset management information system(s). The system(s) shall be designed and maintained to provide an adequate support and information to the organization in meeting all of the requirements set out in clause 4 of this specification. It shall include provision to support the development and implementation/achievement of the asset policy, strategy, risk identification, assessment and control, objectives, targets, plans. It shall also support all of the requirements related to the implementation and operation, checking and corrective actions and the management review.

The information shall be accessible to all relevant employees and other relevant third parties including contractors as appropriate.

Where separate asset management information systems exist, the organization shall ensure that the information provided by these systems is consistent.

However, the requirements do not specify specifically an “electronic-based system” or a computerized system, but the current technology is on using a computerized system that will enable online and real-time information.

To have an excellent information system, the ingredients are as follow, that is:

Be able to perform basic functionalities in asset management and fit for purpose

Be able to interface with existing and future systems

Having excellent data management

Having basic or advance analytical tools

Must be enterprise wide

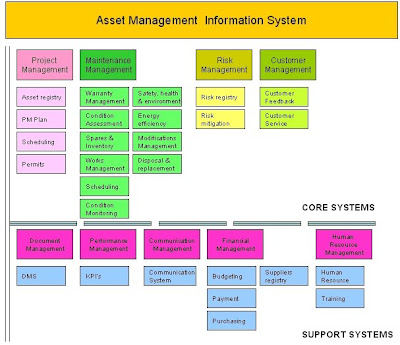

System Functionality

The information system must be able to, as a minimum, to have the functionalities listed in the diagram below:

The organization must also develop an asset identification system to allow a unique identity to each individual asset in the organization. Without an asset registry, there will be no asset management, as we do not know what asset to manage. This is the first function of an information system that needs to be fulfilled before proceeding on to other systems as in the diagram above.

A simple audit will suffice to determine the current position of the organization in the asset management information system maturity model. From this model, a strategic framework on asset management information system will be developed in conjunction with the strategic framework on asset management of the organization.

System Interfacing

The information system must be able to interface with the existing manual or computerized system that is in existence in the organization. During the development phase, decision has to be made to either upgrade or interface with the existing system. This is crucial and the decision has to be made using asset management principles.

It is also worthwhile to look in newer technologies such as Geographical Information System (GIS), Global Positioning System (GPS), real-time condition monitoring system or even Remote Identification System using radio frequency identification device (RFID) and incorporate these technologies in the information system.

The organization has also to look at interfacing of field data from third parties or proprietary equipments/software especially on condition assessment equipments, off site or field measuring equipments, mobile field scanners, hand-held inputting device and so forth.

An information system without interfacing capabilities will be not be an effective system.

Data Management

The integrity of data must be ensured at all stages of collection and inputting of data. Introduction of a specific process in data collection and input will ensure the following, that is:

Correct data is collected and inputted

The data has economic value to the system and organization

Accurate data at all times.

The integrity of data is important and the organization must ensure at all times the data integrity is maintained at all stages of the data recognition, collection and inputting into the system. The best information system will fail if the data collected has no value and inaccurate, as the information system will give false reports and hence, false information. By having a specific process to handle data, the information system is ensured to have the level of data accuracy as desired.

The organization will also have to make a decision on the level of details that the organization needs, as every data is specific to each organization. Nevertheless, external factors also will determine the extent and depth of the details needed. The external factors are:

Legal compliance

Clients requirements

Government requirements

The above requirement can be done through an in-depth study of the external factors and the impact it has on the information system. Beside this, it is equally important to undertake a study on the user requirement before proceeding to the next phase of development of the proposed information system. These two (2) studies have to be done simultaneously in order to have the highest impact on the proposed information system

Analytical Tools

An information system without any analytical generated reports will only be a data reporting system and not an information system. Having this in mind, amongst the basic analytical tools to be incorporated in the information system are as follows:

Benefit-cost analysis

Life cycle costs

Net present value

Current and Future Trends

Graphical presentations

Modeling tools based on mathematical expressions

The more advanced analytical tools, amongst others are as follows:- Condition monitoring

- Economic models

- Decay models

- Predictive models

By having all the analytical, data can be turned into useful information and key performance indicators can be monitored effectively. Hence, the performance of the organization can be displayed as a graphical and meaningful dashboard to be at every level of the organization.

Enterprise Wide

Lastly, the information must be at enterprise wide and be able to be accessed by all levels of staff involved in asset management. The level of use will have a bearing to the effectiveness of the information system, as the competency on the information system would differ at every level of the organization. In a learning organization, the level of use is not a problem for the organization, as the competency, role and responsibility are clearly specified and documented.

Conclusion

Information system is crucial in providing information for, as follows:

- decision making

- performance management

- continual improvement

- corrective and preventive actions

- management review

- knowledge management

The use of asset management principles is necessary in developing and procuring the asset management information system as the asset management information system is a non-physical asset (which include physical asset such as hardware) that has a service potential to the organization.

home

Fig. 4.8 – relationship between design life, economic life and functional life

Fig. 4.8 – relationship between design life, economic life and functional life

{kind=link}

{kind=link}